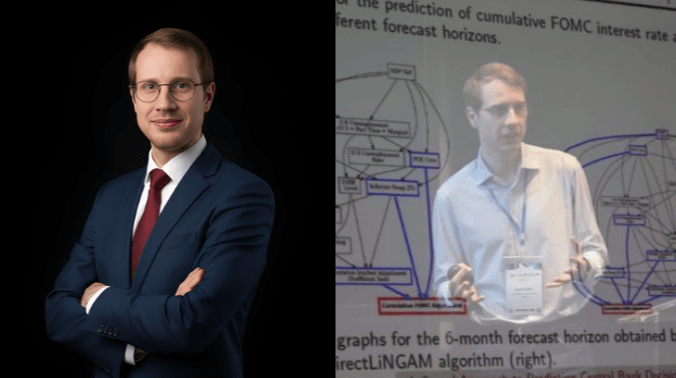

Mathis (ESILV 2022) at the International Risk Forum: Predicting the Fed’s Decisions

On March 30 and 31, 2026, at the 19th Financial Risks International Forum in Paris, Mathis Guenet (ESILV 2022) presented his research on forecasting the decisions of the U.S. Federal Reserve, the body that sets interest rates in the United States.

The Fed’s decisions influence everything: bank loans, investments, and even the global economy. Knowing in advance what it will do helps investors and economists plan more effectively.

His method? Instead of using traditional models, which are often complicated and not always reliable, Mathis used a causality-based approach. In short: he looked for the actual factors that cause rates to change, not just those that appear to be linked. This makes his forecasts clearer and more reliable.

The result? His work shows that we can better anticipate major economic decisions by combining finance and data science, and that understanding causes rather than mere correlations is the key.

Alumni Profile: Mathis, a Product Manager at SCALNYX and a Ph.D. candidate at the De Vinci Research Center (DVRC), graduated from ESILV (Class of 2022) with a degree in financial engineering. He combines quantitative finance, causal artificial intelligence, and macroeconomic modeling. His work spans several areas: portfolio optimization, ESG performance attribution, the creation of predictive financial signals, and anomaly detection in complex time series. He has also contributed to academic projects in deep learning for the calibration of financial models and to the publication of white papers on causal AI applied to finance.

An alumnus to watch!

Comments0

Please log in to see or add a comment

Suggested Articles